Looking back at 2025, early in the second quarter, some Memory Manufacturer discontinued the production of older-generation DRAM products such as LPDDR4X and DDR4, retaining only a few production lines to meet the needs of long-term customers. As a result, supply plummeted, leading to a strong rebound in the spot market prices of server, commercial, and channel DDR4 modules, as well as LPDDR4X products. In the fourth quarter, server demand surged, releasing massive orders. Some customers even locked in capacity for the next one to two years at high prices. OEMs strategically shifted more production capacity toward the server market, simultaneously reducing supply for the domestic consumer segment. Consequently, the spot Memory market experienced multiple rounds of sharp and consecutive price increases across both the resource and finished product segments, with cumulative quarterly (QoQ increases) reaching as high as 1 to 3 times in Q4 alone.

From the perspective of price indices, in March 2025, several OEMs issued price increase notices to channel customers, driving a slight overall increase in spot Memory prices. In the second quarter, prices for DDR4 chips and related finished DDR modules, as well as embedded LP4X, rose, leading to a significant expansion in the increase of the DRAM price index. By the end of the first half of the year, the cumulative increase exceeded 50%. In contrast, the NAND price index rose by less than 10%. The fourth quarter saw an unprecedented wave of price increases across the spot Memory market, driving rapid and sharp jumps in both DRAM and NAND price indices. The quarterly increases for both exceeded 150%, while the annual increases reached as high as 386% and 207%, respectively.

Flash Wafer and DDR chip prices remain unchanged for now.

Flash Wafer Latest Quotations

DDR Latest Quotations

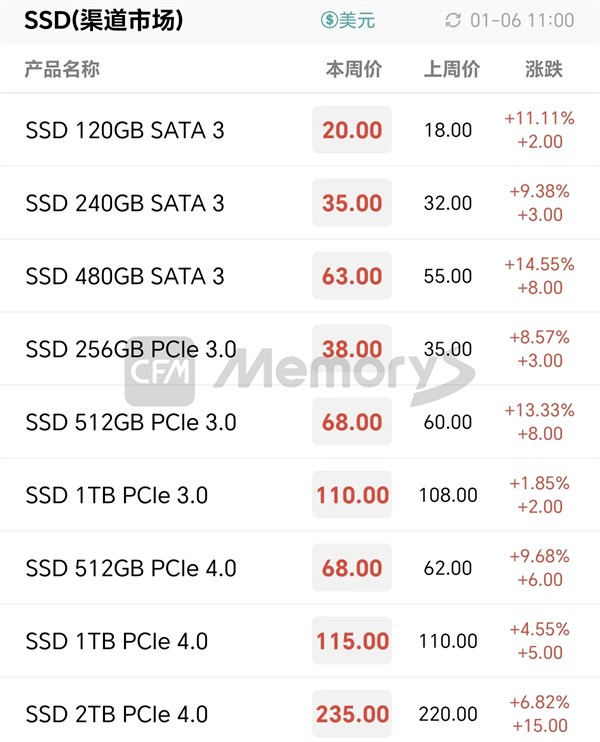

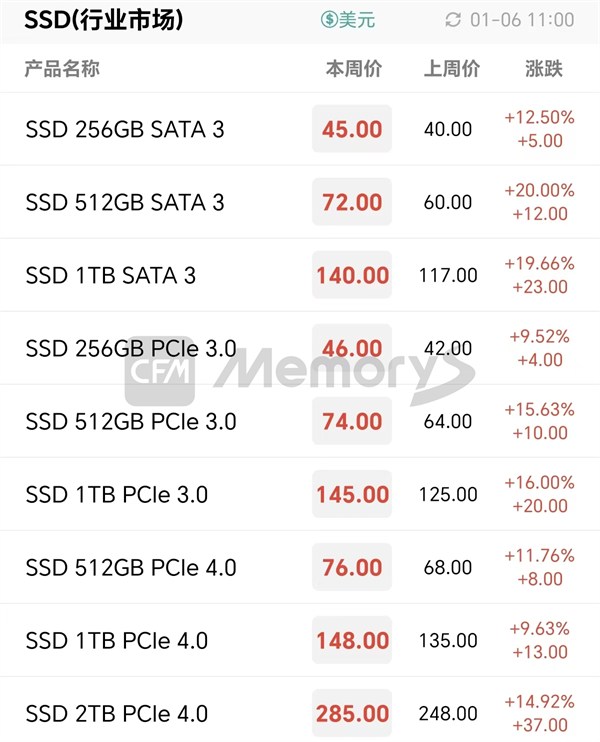

Since the fourth quarter of last year, OEMs have generally implemented substantial month-on-month price increases for NAND resources supplied to downstream Memory manufacturers. Price increases in the channel market resource trade have been even more dramatic. Except for some Memory manufacturers that have formed strategic partnerships with OEMs, others find it relatively difficult to stock up due to excessively high trade-side prices. The upward trend for both NAND and DRAM resources, including lower-end resources, continues. Channel manufacturers are becoming more cautious about pricing and allocation of finished products. SSDs and finished DDR modules are primarily allocated to support core customers such as PC OEMs, with their prices being continuously adjusted upward in line with rising costs. Other customers must accept higher quotations.

Channel SSD Latest Quotations

Channel DDR Module Latest Quotations

In December, the average selling price (ASP) for newly procured 1Tb NAND Wafer contracts by commercial manufacturers approached $0.15, while the ASP for 512Gb NAND exceeded $0.20. Facing continuously rising production costs driven by increasing resource prices, commercial manufacturers are simultaneously raising their product pricing for the new quarter. Currently, some PC OEM customers have accepted the new quarterly price hikes. However, as some PC customers have requested large volumes, commercial manufacturers are strictly controlling allocations considering potential future supply instability. Regarding DDR modules, from the resource side, most high-grade DDR4 chip prices are too high, making it difficult to find supply sources at reasonable price points. Currently, some commercial manufacturers prefer to purchase certain amounts of lower-grade resources to replenish inventory. As finished products using these lower-grade resources offer relatively better pricing, this can alleviate some of the hardware cost pressure for PC manufacturers to a certain extent.

OEM SSD Latest Quotations

OEM DDR Module Latest Quotations

Since the fourth quarter, despite OEMs actively allocating DRAM production capacity to the server market, the new server DDR5 demand from North American Cloud Service Providers (CSPs) has far exceeded expectations. More North American CSP customers are willing to pay high premiums to secure supply priority. However, with current OEM production capacity, it is difficult to fully cover the large-scale additional order demand. Server DDR module prices continue to jump. This month, prices for server 32GB/64GB/96GB DDR5 RDIMM are $380/$720/$1300 respectively, while prices for 16GB/32GB/64GB DDR4 RDIMM are $260/$350/$650 respectively.

Server DDR Module Latest Quotations

OEMs are actively upgrading NAND production lines to higher-layer 200+/300+ technologies. The output of 1Tb/2Tb NAND Wafers is gradually increasing, while 512Gb NAND Wafer resources are significantly shrinking. Some OEMs have essentially stopped supplying 256Gb NAND. Memory manufacturers have limited old inventory left, leading to tighter supply. This week, prices for small-capacity eMMC continue to be raised, while prices for large-capacity eMMC and LPDDR4X remain unchanged for now.

eMMC Latest Quotations

eMCP Latest Quotations

LPDDR Latest Quotations

UFS Latest Quotations

uMCP Latest Quotations

All Rights Reserved © 2026 MemoryMarket.com