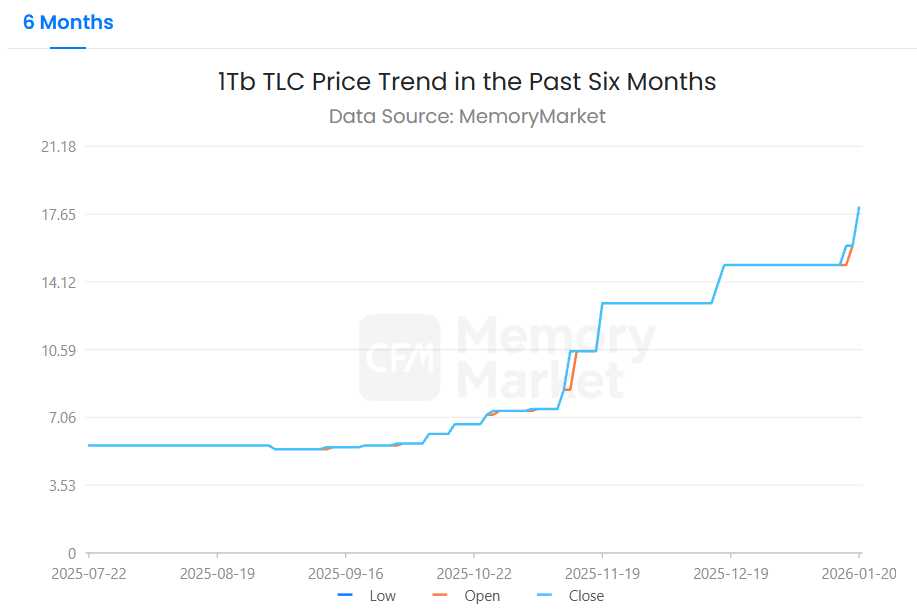

Recently, some original manufacturers have released spot NAND resources to downstream memory manufacturers, with prices for certain products surging over 30% month-on-month. Driven by frequent and aggressive month-over-month price hikes from the supply side, the cumulative increases for 512Gb/1Tb TLC NAND and 1Tb QLC since the fourth quarter of last year have already reached as high as 200–300%.

Since the fourth quarter of last year, as NAND resource prices have continued to climb, downstream memory manufacturers initially relied on existing low-price inventories to buffer cost pressures. However, after months of consecutive sharp price increases and amid unpredictable future trends, manufacturers are now placing greater emphasis on cost control, closely monitoring the prices of newly procured resources, and reflecting these costs in corresponding finished products. Currently, high-priced industry and channel SSDs, as well as embedded products, have indeed dampened some demand-side stocking willingness, leading to a noticeable contraction in shipment volumes. Nevertheless, overall revenue levels remain high, largely due to significant increases in product selling prices. It is crucial to be vigilant: if memory product prices exceed a certain threshold, they may trigger greater resistance from customers.

In terms of upstream resources, the prices for 1Tb QLC, 1Tb TLC, 512Gb TLC, and 256Gb TLC have been adjusted to $17.00, $18.00, $15.00, and $9.00 respectively today, while DDR chip prices remain unchanged for now.

Flash Wafer Latest Quotations

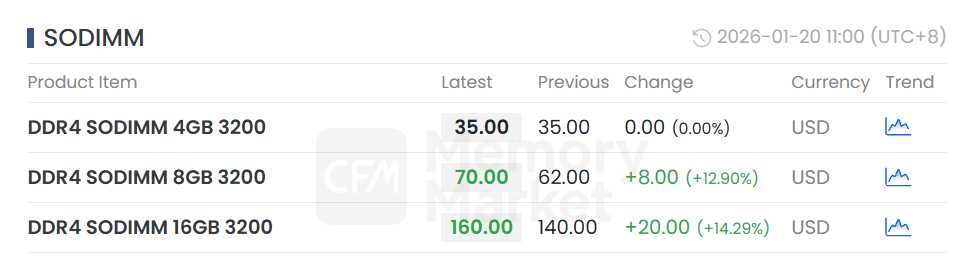

DDR Latest Quotations

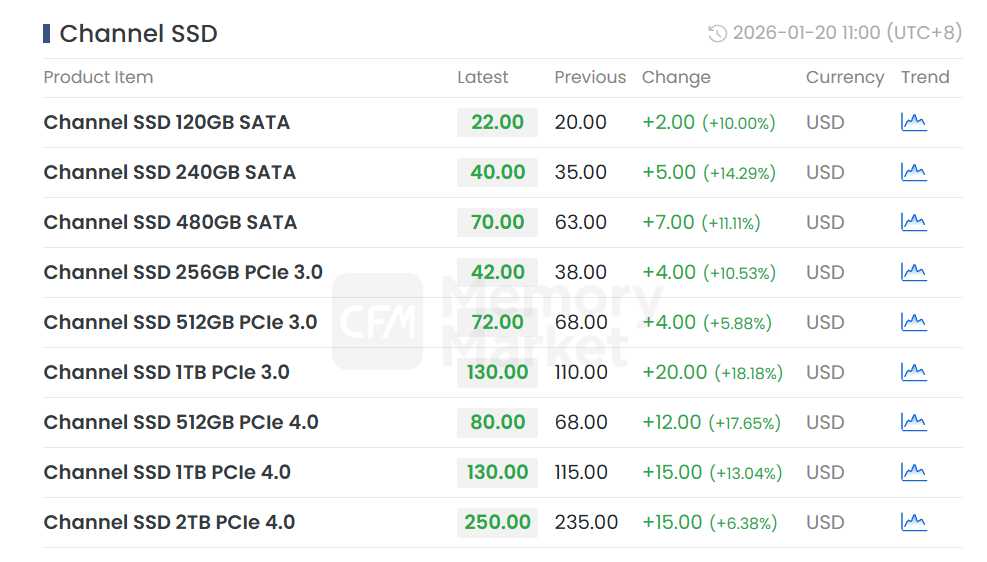

In the channel market, prices for DRAM and NAND—including low-end resources—are rising across the board. With resource costs remaining persistently high, channel manufacturers are forced to raise finished product prices. This week, channel SSD and DDR module prices have increased. After multiple rounds of adjustments, current channel SSD and DDR module prices have reached all-time highs. Although procurement demand from channel customers has significantly contracted, in this environment of shrinking volume and rising prices, the price increases partly offset the decline in transaction volumes.

Channel SSD Latest Quotations

Channel DDR Module Latest Quotations

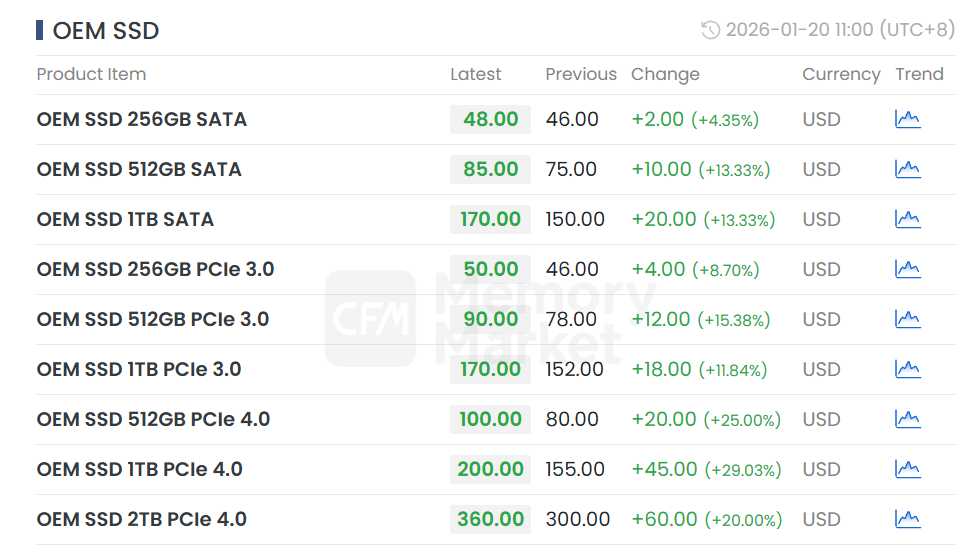

Since the fourth quarter of last year, original manufacturers have aggressively driven up NAND Flash prices. This month alone, 1Tb NAND resource prices have surged by as much as 20%. Industry manufacturers are increasingly focusing on the cost pressure that real-time dynamic prices of newly procured resources impose on finished products, and they are reflecting these increases to the finished product end based on current resource prices. This week, industry SSD and 8GB/16GB DDR4 module prices continue to rise. Judging from the attitudes of demand-side releases, industrial control and specific application scenario industry customers show relatively high acceptance of current high prices, while some PC customers find them difficult to bear.

OEM SSD Latest Quotations

OEM DDR Module Latest Quotations

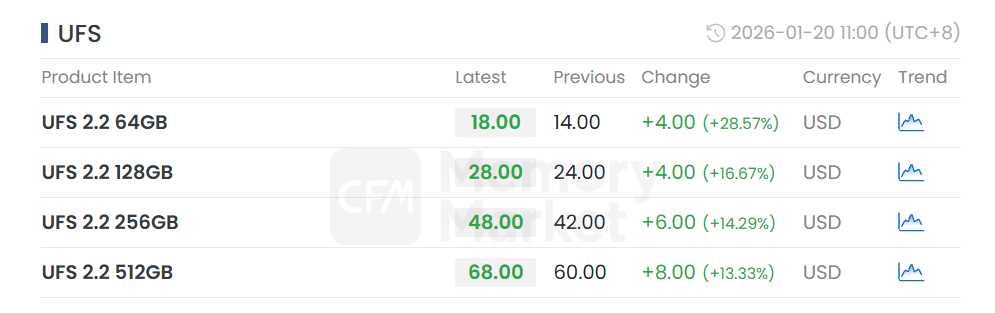

Breaking down by capacity, 64GB and lower capacities face tighter finished product supply due to resource shortages, driving continuous price increases for low-capacity eMMC. Meanwhile, large-capacity eMMC prices are rising rapidly as resource costs push further upward, compounded by capacity reduction at the application level, making shipments of large-capacity embedded products even more challenging. Some products have even fallen into a situation of "having prices but no market." This week, embedded eMMC and UFS prices have been adjusted upward across the board following the rise in NAND resource prices, with corresponding integrated products following suit.

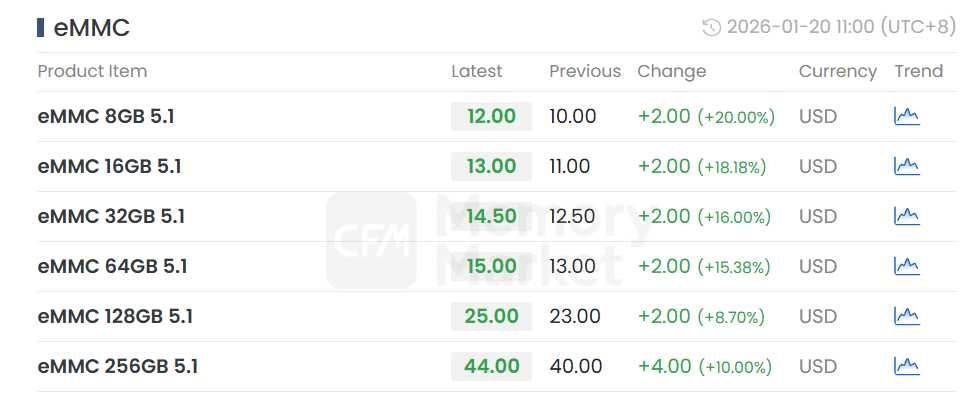

eMMC Latest Quotations

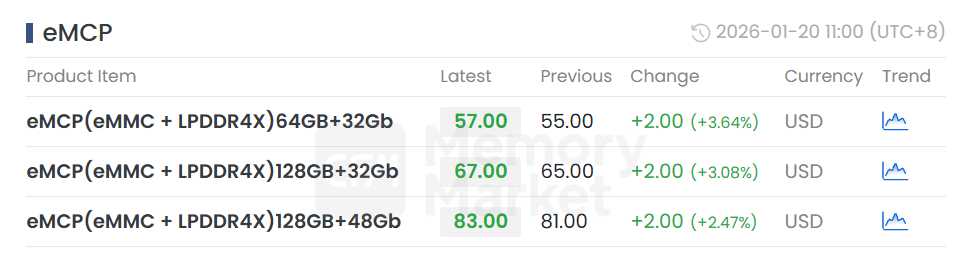

eMCP Latest Quotations

LPDDR Latest Quotations

UFS Latest Quotations

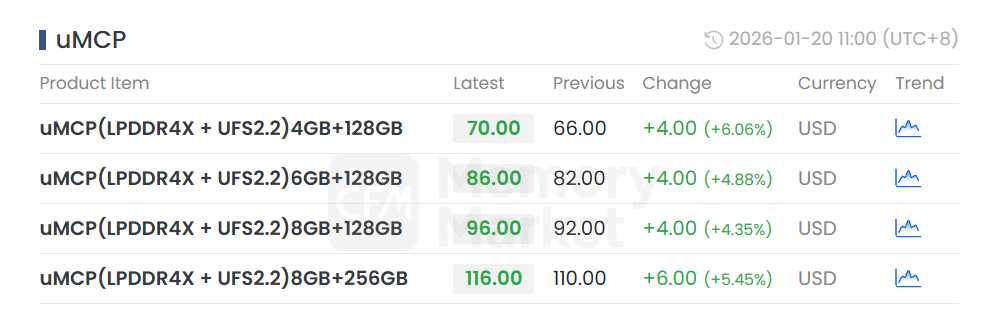

uMCP Latest Quotations

All Rights Reserved © 2026 MemoryMarket.com