Currently, except for a few Memory Manufacturers offering temporary quotes to specific end customers, the market is generally still in the new quarter allocation phase, and the actual price increases for most products have not yet been finalized. Memory Manufacturers continue to maintain a supply-control stance, with new-quarter NAND Wafer allocations and pricing yet to be released. High-grade DRAM resources are accessible only to a very limited number of memory companies, while most manufacturers have not received supply for several months. Amid continuous price hikes and unstable supply, memory suppliers are largely accepting orders cautiously based on confirmed demand and agreed prices.

However, acceptance of these price increases varies across the spot memory market. Industrial PC, industrial control customers, and channel PC system integrators generally show higher acceptance. In contrast, non-core customers, who are more price-sensitive, now face higher procurement costs, which has significantly dampened their willingness to build inventory. In terms of capacity, some application markets are shifting toward lower specifications and capacities. Whether in industrial, channel, or embedded products, higher-capacity items face greater shipment pressure compared to lower-capacity ones. With clear upward momentum in resource pricing, the overall trend of finished products being pushed up passively by costs is unlikely to change in the short term, and it will take time for more customers to accept the new price levels.

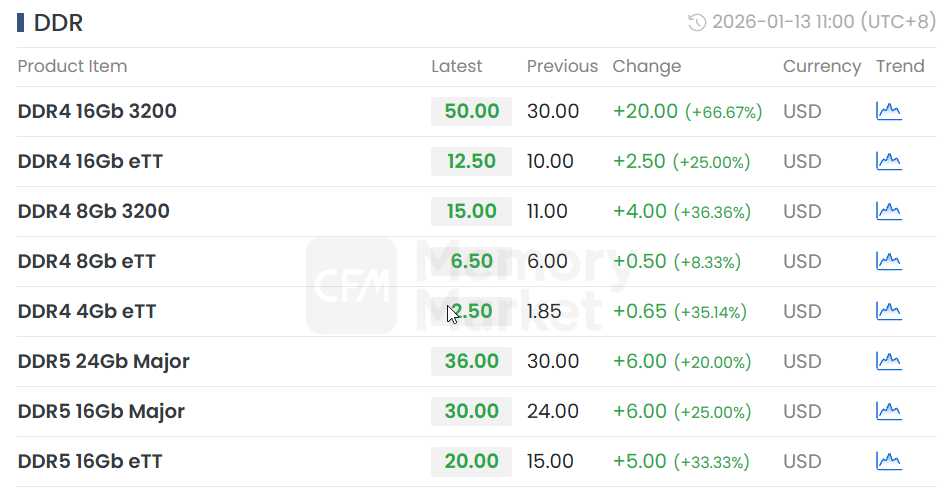

On the upstream resource side, Flash Wafer prices remained unchanged today. This week, most DDR chip prices rose sharply:

DDR4 16Gb 3200 / 16Gb eTT / 8Gb 3200 / 8Gb eTT / 4Gb eTT increased to USD 50.00 / 12.50 / 15.00 / 6.50 / 2.50 respectively.

DDR5 24Gb Major / 16Gb Major / 16Gb eTT increased to USD 36.00 / 30.00 / 20.00 respectively.

Flash Wafer Latest Quotations

DDR Latest Quotations

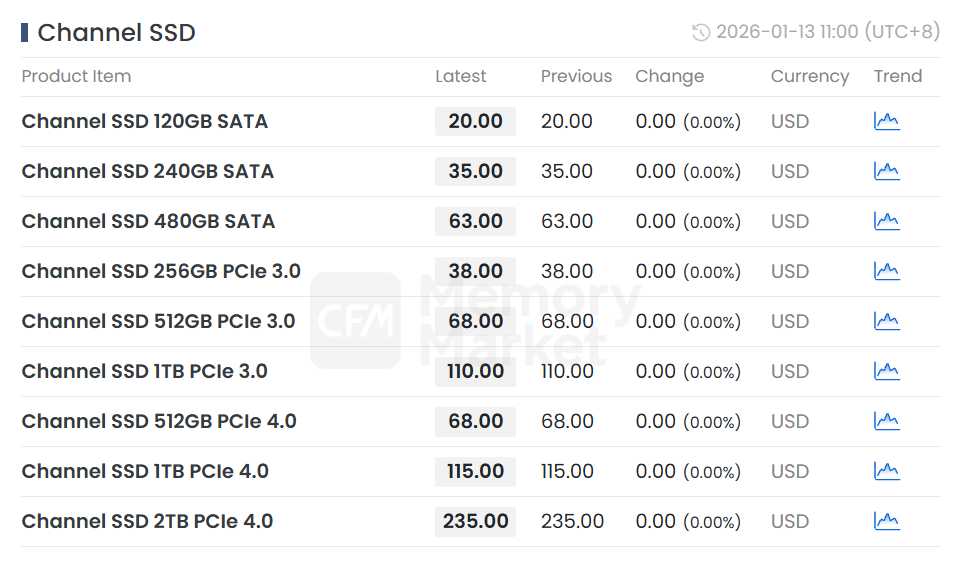

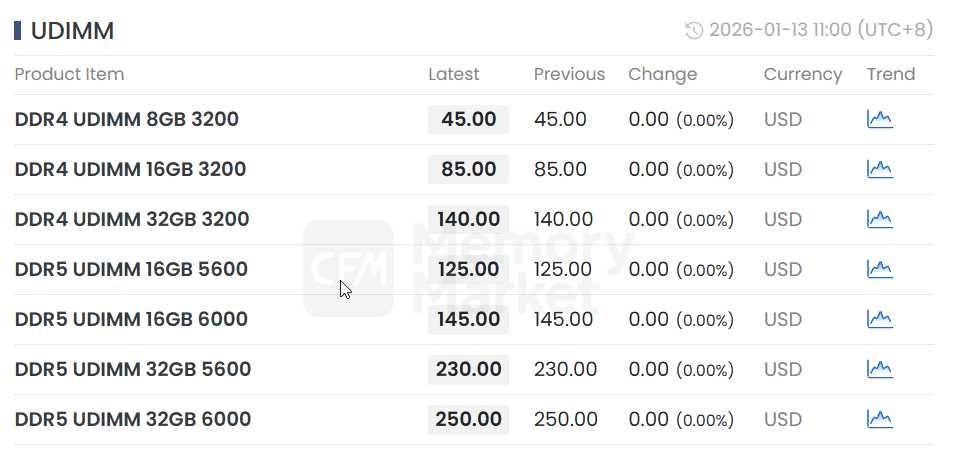

Since Q4 last year, the channel market has repeatedly raised prices passively following rising resource costs. However, in actual shipments, some non-channel system customers struggle to accept the current high prices, and with existing inventory on hand, the market still needs time to digest and gradually adapt to the new price levels. This week, prices for Channel SSDs and DDR UDIMM remained stable.

Channel SSD Latest Quotations

Channel DDR Module Latest Quotations

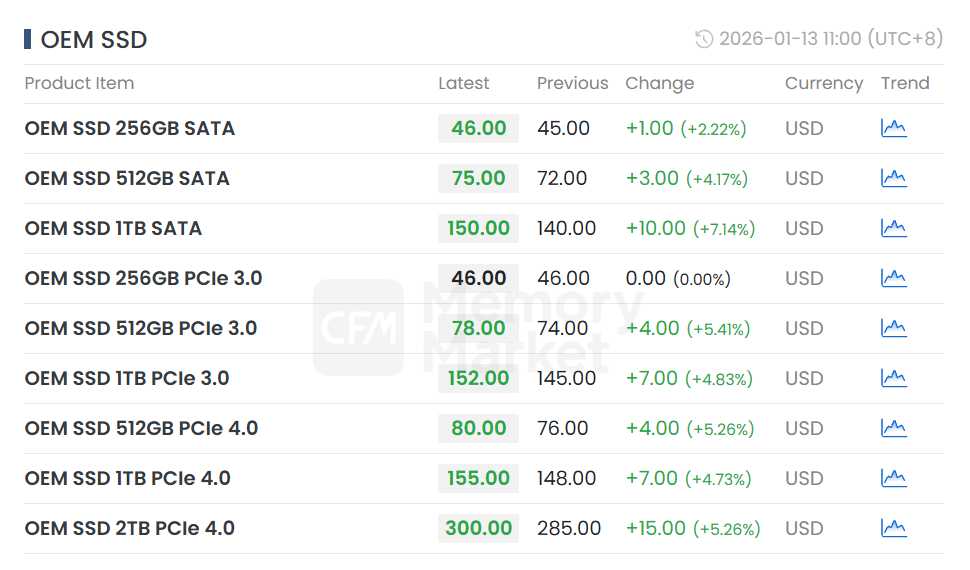

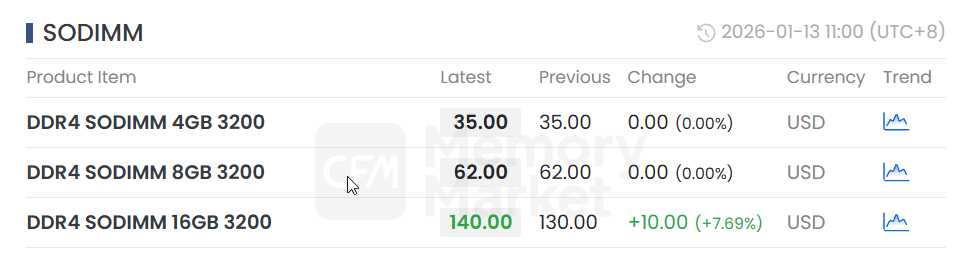

Although some PC OEMs have turned to industrial suppliers due to insufficient support from Memory Manufacturers’ supply strategies, the successive price increases in DRAM and NAND resources have driven up corresponding finished product costs. With PC hardware costs rising significantly, PC makers are now more inclined to purchase lower-capacity memory products. Currently, allocations and pricing for some key PC OEM customers have been negotiated, though available inventory remains limited. Industrial suppliers continue to raise quotes, mainly accepting small-batch orders. This week, prices for OEM SSDs and 16GB DDR SODIMM increased slightly.

OEM SSD Latest Quotations

OEM DDR Module Latest Quotations

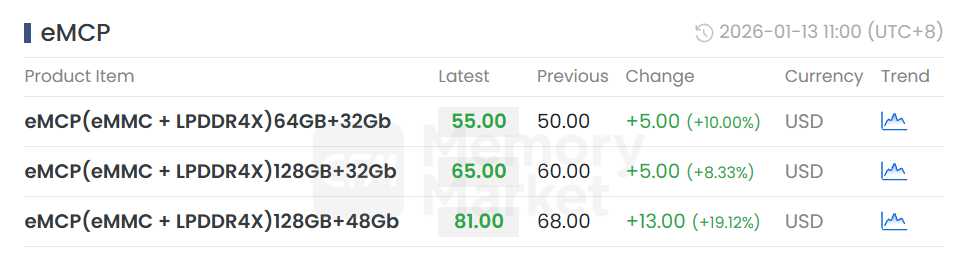

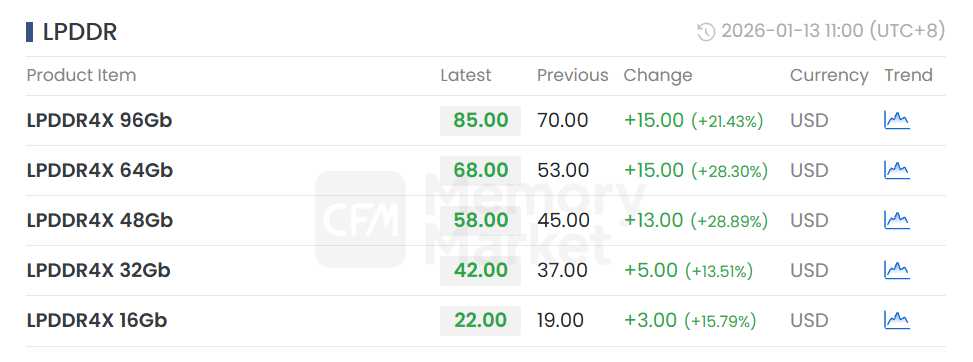

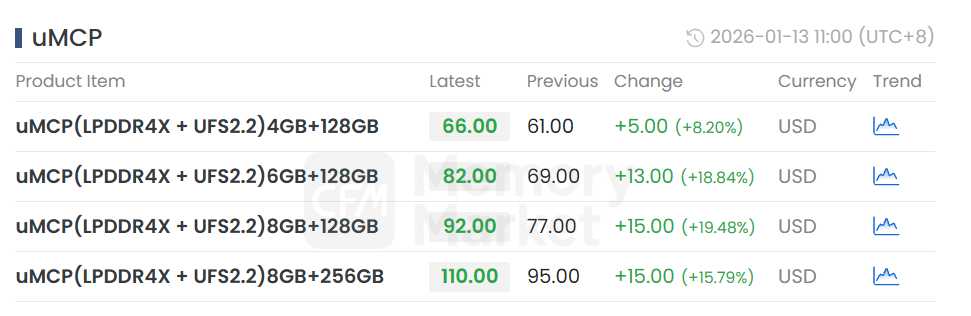

Recently, it has been reported that some Memory Manufacturers provided temporary Q1 quotes for LPDDR4X to mobile customers, reflecting a sequential increase of about 40%. Final settled prices are still undetermined. Notably, in Q4 last year, production costs for some memory companies even exceeded these quoted levels. Given that LPDDR4X resource prices are expected to rise further in Q1, memory suppliers with previously low inventory levels will see significantly narrowed profit margins for shipments to Tier‑1 customers this quarter. Currently, there is a noticeable price gap between major core customers and non‑Tier‑1 customers, posing considerable pricing challenges for memory companies. The situation where “flour is more expensive than bread” remains difficult to improve. Coupled with widespread market expectations for further price increases, memory suppliers have comprehensively raised LPDDR4X product prices this week, with related integrated products following the upward trend.

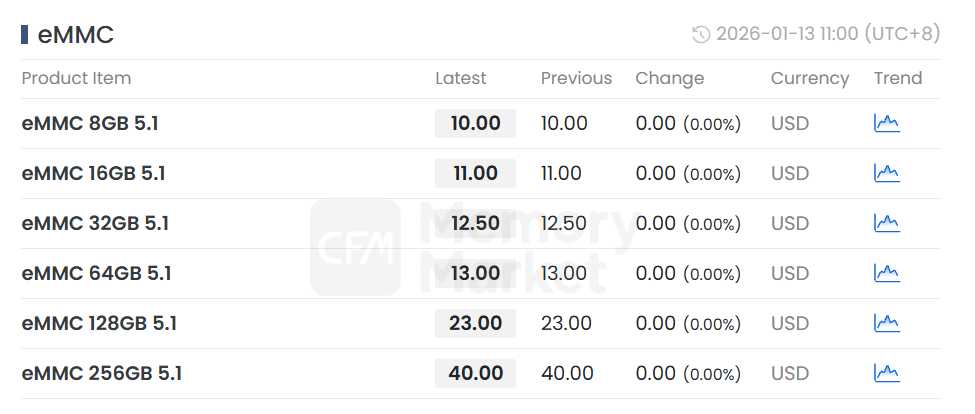

eMMC Latest Quotations

eMCP Latest Quotations

LPDDR Latest Quotations

UFS Latest Quotations

uMCP Latest Quotations

All Rights Reserved © 2026 MemoryMarket.com